If there’s one thing most people don’t think about until they really need it, it’s insurance. Yet behind every policy, claim, or form is a sprawling set of workflows that still might feel more like relics for most of the industry. Despite decades of technological progress across business sectors, insurance continues to lag in the very areas where efficiency, accuracy and customer experience matter most.

To understand why this matters, it helps to look at how the insurance innovation is evolving – and where it’s stuck.

Challenges of insurance platform development

Even though the global insurance industry is acknowledging the need for digital transformation, adoption is still uneven. According to the 2025 ACORD Insurance Digital Maturity Study, only about 25% of insurers have fully digitalized their value chains. More than half are still exploring how digital fits their business model, and over 10% haven’t leveraged these technologies in meaningful ways at all.

The legacy system burden

To put it bluntly: many insurers today operate on technologies that were created long before the internet was central to business. These legacy systems are expensive to maintain, hard to integrate, and slow to evolve. They were not designed for the real-time, API-centric world that modern insurance portals require.

In fact, data from market analysts shows up to 70% of an insurer’s annual IT spend goes toward maintaining legacy platforms, leaving far less for innovation in life insurance. The same research points out that digital and AI integration could cut annual operating costs by as much as $300 billion in life insurance alone.

Older platforms are not only costly but also rigid. Even small changes, like modifying a single data field, can require rebuilding thousands of program components. That dramatically increases the time and effort required to launch new products or comply with regulatory requirements.

Integrability and interoperability issues

Insurance organizations often manage data and processes in siloed systems, each functioning as its own isolated entity. Not only this fragmentation impairs data visibility, making it difficult to get a unified view of customer activities or risk profiles, but also hampers the integration of new services such as advanced analytics, AI-powered decisioning, or third-party microservices.

Modern software, by contrast, strive for integration that enables end-to-end automation, seamless partner connectivity, and real-time workflows. These attributes are difficult to retrofit onto older systems without deep architectural re-engineering.

Regulatory and compliance pressures

Insurance, perhaps more than many industries, operates under stringent regulatory frameworks that govern how data is collected, stored, and processed. Laws like GDPR in Europe and others in key markets such as the United States mandate strict rules around privacy and consent, particularly pertinent for life insurance where sensitive personal health information is involved.

Beyond life insurance technology itself, process inefficiencies continue to constrain insurers. For example, surveys of industry leaders suggest that it often takes more than five months to implement regulatory rule changes, with nearly a fifth of firms taking over seven months. Therefore, compliance and product updates are not keeping pace with business needs.

Organizational and cultural barriers

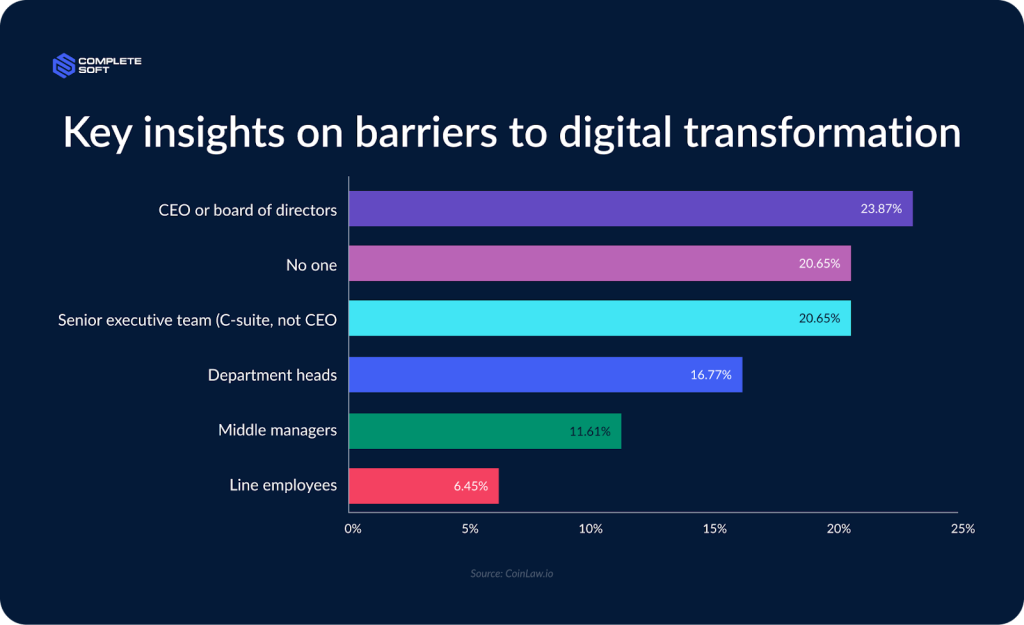

Often overlooked in technology discussions is the human dimension of digital transformation. Within many insurtech companies, there remains significant cultural resistance to change. It’s partly rooted in the long success of established processes and partly due to apprehension about disrupting familiar workflows.

Without the right organizational readiness, even the most promising technological investments can stall or underperform.

Talent gaps and skills shortage

Meanwhile, many insurers struggle with talent. While digital skills are essential to transformation, only about 35% of insurers believe they have the internal resources necessary to drive that transformation forward.

Advanced platforms require teams proficient in data architecture, cloud engineering, API design, security practices, and modern software delivery. Yet many insurers find themselves competing with tech firms for talent that is in short supply.

Rising customer expectations

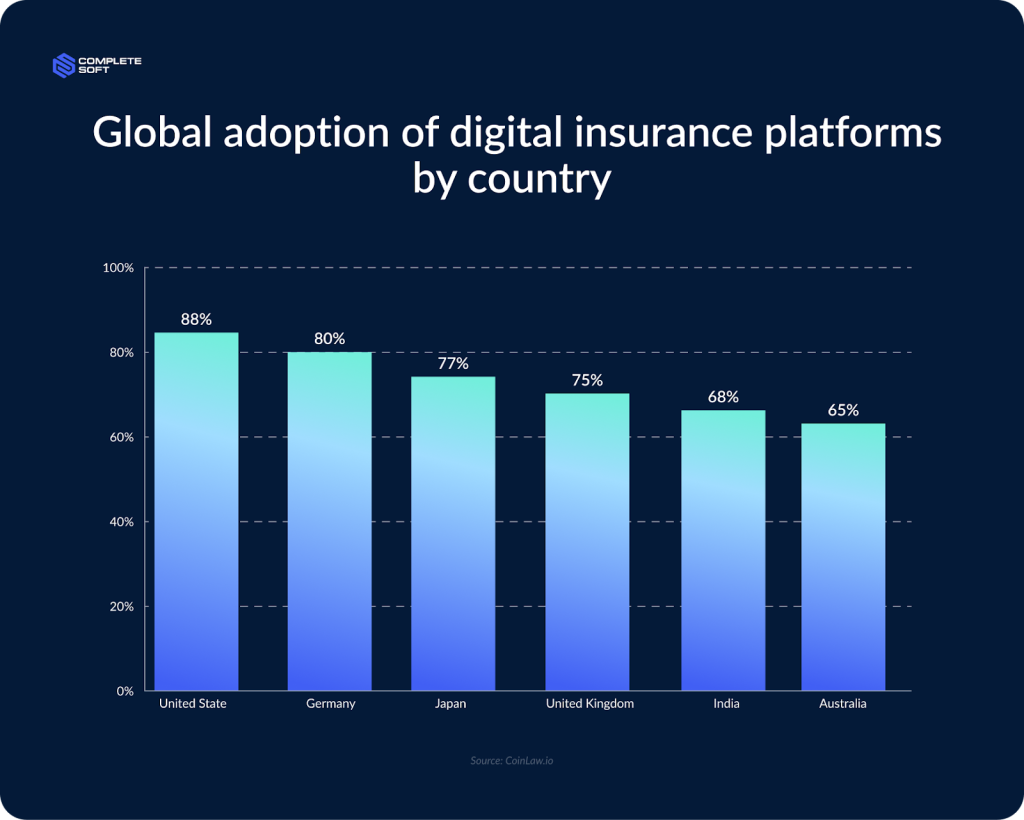

Finally, the pulse of the end user cannot be ignored. Policyholders today expect fast, intuitive, and digital experiences much like they receive from consumer-tech platforms. Whether it’s completing an application online, signing a document digitally, or checking policy status via mobile app, these experiences are table stakes. For example, studies show 70% of insurance customers prefer digital channels over traditional agents, and 54% of policies are now sold online.

Legacy systems (clunky UIs, slow processing, manual handovers) often fail these expectations, leading to frustration, drop-offs during application flows, and even churn. Research from Accenture shows that 79% of customers would switch providers for better digital service.

Fortunately, there is a solution: thoughtfully designed, standards‑based, and developer‑driven smarter insurance platforms. Here, CompleteSoft is sharing its experience in delivering such solutions.

Wondering whether your current insurance platform is still fit?

If so, you’re welcome to reach out. We’re always open to a free, informal conversation to look at things from a technical and practical perspective.

Core principles for building smarter insurance platforms

Looking across different transformation initiatives, a few patterns tend to repeat themselves. They are less about life insurance technology trends and more about architectural choices that either make systems easier to evolve or quietly hold them back over time.

Modularity over monoliths

One consistent lesson is that tightly coupled systems don’t age well. As insurance products, regulations, and partner integrations change, monolithic platforms become increasingly resistant to modification.

Modular architectures (where document processing, underwriting logic, digital signatures, and analytics can evolve independently) make change less risky and less expensive. They also create room for ecosystems: integrating external services without deep, custom point-to-point connections.

An API-first approach often becomes the practical foundation here, not because it is fashionable, but because it forces clearer boundaries between system responsibilities.

Scalability as a design assumption

Modularity naturally leads to questions of scale. Insurance workloads are uneven: document generation, form submission, or signature flows can spike dramatically at certain points in the business cycle.

Cloud-based and microservice-oriented designs allow individual components to scale independently and recover gracefully from failure. In practice, this means that document-heavy processes don’t overwhelm the rest of the platform which is an important consideration for life insurance systems that generate and process large volumes of customized forms.

Integration is not optional

Insurance platforms rarely operate on their own. They depend on CRM, billing engines, underwriting tools, medical data providers, and external partners.

Treating integration as a secondary concern almost always leads to manual workarounds later. Platforms that assume continuous, real-time data exchange from the outset tend to support smoother automation and better visibility across processes. Standardized data models and clearly defined interfaces make this possible without constant rework.

Compliance and security are architectural concerns

In regulated environments, compliance cannot be layered on at the end. Life insurance platforms handle sensitive personal and medical data, and they are expected to withstand audits, legal review, and long retention cycles.

That reality shapes architecture decisions early on: encryption, access control, audit trails, and traceability are part of the system’s core behavior. When handled thoughtfully, they protect both customers and the business.

User experience affects operational outcomes

Insurance forms are still often complex. When interfaces are confusing or slow, the result is user frustration which leads to incomplete data, processing delays, and additional manual effort downstream.

Data becomes valuable only when it’s trusted

Most insurance organizations already have plenty of data. The challenge is consistency, quality, and accessibility.

Software that consolidates data across systems (and applies governance early) are better positioned to support data analytics in the insurance sector, underwriting decisions, and future automation. Without reliable foundations, more advanced capabilities still remain theoretical.

Change is continuous

Finally, insurance platforms are never finished. Regulations evolve, products change, and business priorities shift.

Teams that invest in continuous delivery, automated testing, and disciplined release processes tend to move forward with fewer disruptions. In contrast, systems that resist incremental change often require costly, disruptive rewrites later on.

Lessons from real-world development (CompleteSoft track record)

Abstract principles only become meaningful when they collide with real constraints: legacy infrastructure, regulatory frameworks, tight timelines, and users who just want things to work. Over the years, CompleteSoft has been involved in developing and evolving several life insurance document-processing and automation systems for the US market.

Below are some of the most important lessons drawn from hands-on development experience.

Life insurance application processing system: complexity starts with “simple” forms

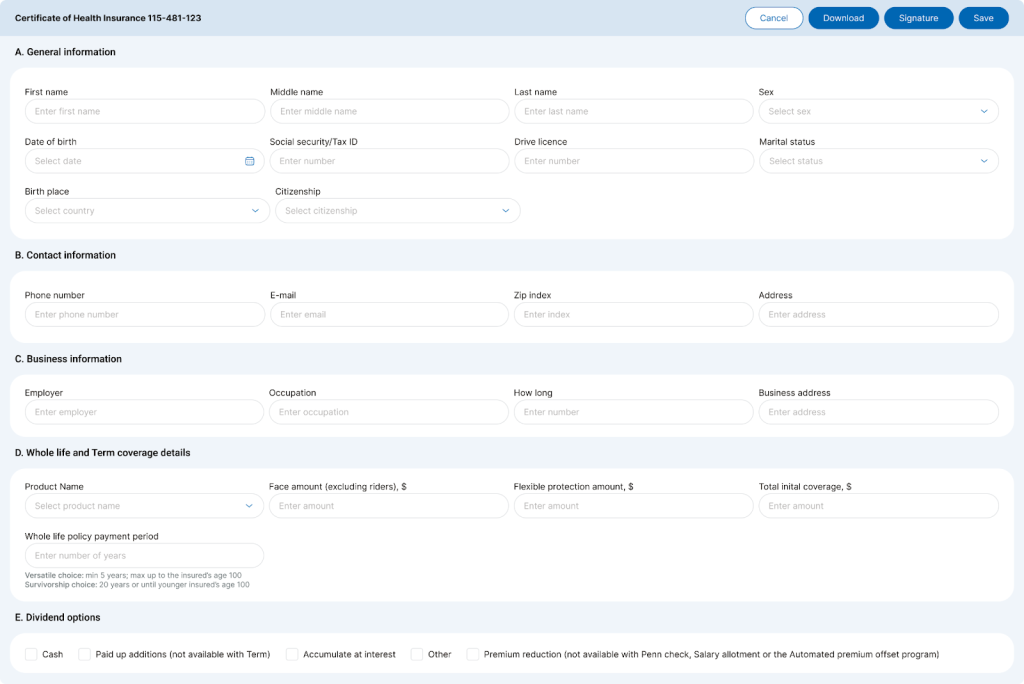

At first glance, the goal of the life insurance application processing system sounds straightforward: provide insurers and agents with a web-based way to fill out life insurance forms, sign them electronically, and generate legally valid documents.

In reality, this task quickly unfolds into a complex orchestration of business rules, standards, and integrations.

The system was designed to support the first stage of the life insurance business process in the US, offering:

- Dynamic sets of visual forms that vary depending on the product and process type

- Secure electronic signature workflows

- Generation of images and PDF documents

- Compliance with ACORD standards, widely used across the US insurance industry

- Electronic document exchange with external life insurance systems

One of the first challenges was dealing with form variability. These applications are not static templates. They change based on underwriting requirements, state regulations, product configurations, and client data. This required a flexible form engine, capable of rendering and validating different form sets without rewriting core logic every time a rule changed.

Another critical insight was the importance of electronic signature reliability. In regulated environments, an e-signature is a legal artifact. That means clear audit trails, secure authentication, and predictable behavior under edge cases (such as interrupted sessions or partially completed forms).

UComplete and ExamComplete

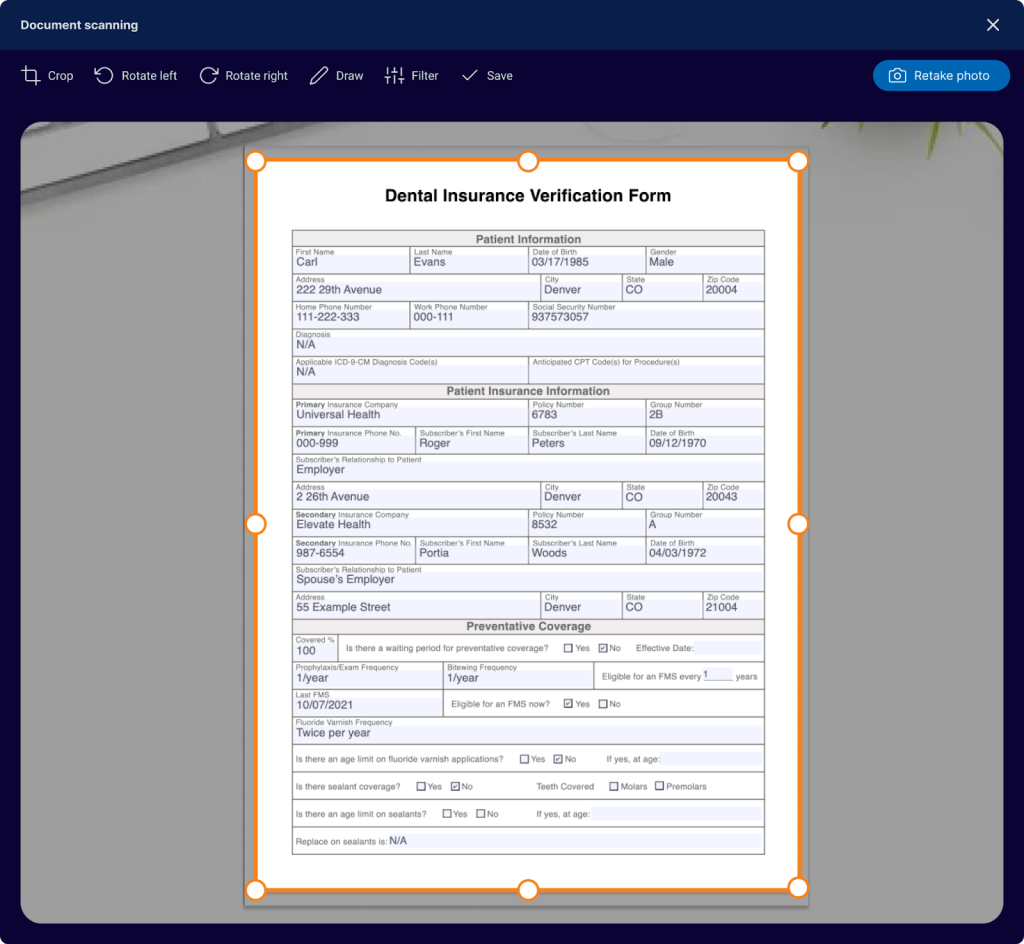

Other projects we’ve worked on, UComplete and ExamComplete, addressed another pain point: manual effort during application and medical data collection.

UComplete automated the completion of base insurance forms, integrating electronic signatures and document scanning.

And ExamComplete focused on medical forms, where accuracy, data consistency, and compliance are especially critical.

Here, the challenge was less about raw document generation and more about workflow optimization. Agents and underwriters don’t want to fight the system, they just want it to quietly remove friction from their daily tasks.

Two insights stood out:

- Automation must respect existing business processes

Replacing paper with digital workflows doesn’t automatically make a process better. In several cases, success came from carefully mapping how agents already worked and then automating around those patterns, rather than forcing entirely new ones. - Integration beats isolation

Scanning systems, electronic signatures, and form engines only delivered real value once they were fully integrated. Partial automation often created more confusion than clarity. End-to-end workflows (from form completion to signed, archived documents) were what actually reduced errors and rework.

Read a detailed case study about ExamComplete development process!

What these projects taught us overall

Working on life insurance document processing and automation platforms for the US market has consistently shown us that successful systems are built less on bold promises and more on disciplined engineering choices. Below are the key lessons that emerged across multiple projects:

- Document processing sits at the center of insurance workflows.

Systems that treat documents as structured, rule-driven entities tend to remain stable longer and adapt more safely to change. - Flexibility is more valuable than an extensive feature set.

Platforms built around configurable forms and clearly separated business logic are easier to maintain than those relying on rigid, hard-coded behavior. - Industry standards reduce friction rather than add constraints.

Aligning with standards such as ACORD simplified integration, reduced ambiguity in data exchange, and helped maintain consistency across platform components. - Electronic signatures demand more than surface-level implementation.

Reliable implementations require careful handling of identity, auditability, and edge cases. When this rigor is missing, trust and compliance quickly become concerns. - Integration works best when it is designed in from the start.

Insurance portals depend on constant interaction with other systems. Clear interfaces and consistent data models proved far more resilient than integrations added later under operational pressure. - Automation is effective only when it aligns with real workflows.

In practice, the most valuable automation reduced friction in existing processes rather than replacing them entirely. - User experience directly influences data quality.

Clear, adaptive interfaces helped reduce incomplete or inaccurate submissions.

Manual paperwork consumes hours of staff and teacher time each week.

Digital workflows automate approvals, attendance, reporting, and compliance checks, allowing teachers to focus on teaching instead of forms. Many schools report a 30–50% reduction in time spent on routine documentation after adopting a structured e-document system.

If you’re in the middle of rethinking an insurance platform, or just want to sanity-check some decisions, a fresh technical perspective can be useful. We’re always open to an honest conversation and can offer a free consultation to walk through your challenges and ideas, without any obligation. Feel free to reach out!

FAQ

Can you help if we’re not sure what needs to be changed yet?

Yes. Often the first step is simply understanding where current systems create friction or risk. A short technical or architectural discussion can help clarify options before any decisions are made.

Do you only work with legacy systems, or new platforms too?

Both. Some projects involve modernizing or extending existing platforms, and others start from scratch. In practice, many engagements combine building new components while integrating with legacy systems.

What types of insurance platforms does CompleteSoft work with?

We primarily work with life insurance platforms, especially systems focused on document processing, application workflows, electronic signatures, and integration with external services. That said, many of the architectural principles apply across other insurance domains as well.